Lending Tool To Enhance Real Estate Success

September 19, 2023 | Market Trends

September 19, 2023 | Market Trends

Using a lending product like a 2-1 temporary buydown is a great strategy that gives sellers an edge in making their homes more attractive to buyers by softening the payment shock buyers experience as rates have risen quickly.

In this article we briefly explain current real estate market conditions, how they impact buyers and sellers, and how consumers have been using this 2-1 buydown product to enhance their success.

The biggest challenge facing the Colorado real estate market is the shift in purchasing power for buyers. Mortgage interest rates have increased by almost 5 percentage points in the last 18 months, even as purchase prices have continued to rise. The outcome is very simple: more expensive monthly payments.

In February of 2022, the monthly principal and interest payment on a $400,000 loan at a 3% interest rate was $1,686. The same $400,000 loan today has an interest rate more than twice the old rate and carries a monthly principal and interest payment of roughly $2,797. This increase in payment doesn’t consider other inflationary factors such as property insurance, real estate taxes and all manner of maintenance costs.

Reduced affordability in the form of higher payments and a historically low number of homes on the market have conspired to create the fewest number of homes sold per capita in the history of the Colorado real estate market.

As a result sellers are experiencing longer marketing time, price reductions and offers below asking price. As of mid-September 2023, it takes just over two months for the average property to go under contract, 36% of properties are experiencing a price reduction and 54% of properties are selling for less than the asking price.

Buyers have become more demanding about the homes they purchase (which is a good thing) and sellers are having to find ways to make their homes stand out amongst the competition.

The most powerful tools that have served sellers in the past are still the most important ingredient for an effective sale. Staging, painting, carpet, and curb appeal are strategic investments (along with proper home pricing) that can create an emotional connection with buyers, driving the value of the home higher.

While the emotional connection matters, the more attractive sellers can make a home’s payment, the more desirable the home is for buyers.

Both buyers and sellers have been experiencing success deploying a financial strategy using a mortgage product called a 2-1 buydown.

Sellers who are effectively advertising a home with the offer to pay for this product on behalf of prospective buyers have been successful at attracting buyers to write offers on their property who may not have otherwise.

Buyers benefit by using this product to take a stair-step approach in easing into their new monthly payments.

NOTE: Payments will rise based on the long-term fixed rate, and the buyer is qualified for their mortgage based on this rate. If rates continue to rise, the buyer will be happy they purchased at today’s rate. If rates drop, the buyer benefits by being able to refinance to the lower long-term rate and typically can capture the unused buydown amount as a reduction to their loan principal. Either way, we are recommending real estate purchases in this market as long term acquisitions and for households that have at least 6 months of household expenses in cash reserves.

A 2-1 buy down isn’t the right loan product for every situation, which is why my lending team and I always take a consultative approach to the process of helping buyers and sellers.

Some sellers shouldn’t advertise this product or any concession to a buyer for a myriad of factors such as location, uniqueness and condition of their home. Their home may already be incredibly attractive without needing to offer the buyer additional incentive.

Some buyers will need or want a completely different loan product as a result of credit, loan amount, down payment and other factors.

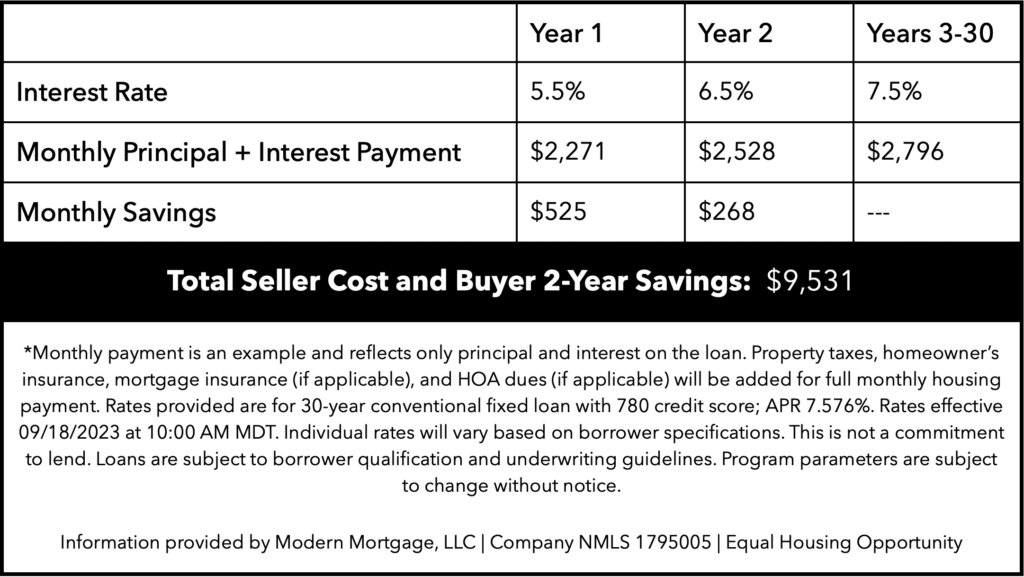

A buyer must qualify for financing at the prevailing interest rate at the time of their loan application. In the example below the buyer is qualified at the rate of 7.5% on a 30-year fixed loan.*

A savvy seller may choose to advertise their willingness to pay for the buydown as a proactive incentive to attract buyers. Note: The real estate agent must ensure compliance with real estate and lending requirements.

The cost of the temporary buydown will vary based on the prevailing interest rate for a particular buyer’s qualifications (down payment, credit profile, and other factors). The cost of the buydown is exactly the same as the buyer’s monthly payment savings over the first two years of the loan. In the example below, the seller would purchase the temporary rate buy down for the buyer at a cost of $9,531. The monthly payment savings to the buyer over the first two years is exactly $9,531.

Why couldn’t the seller just give the buyer $9,531 in cash at closing? Because it’s considered loan fraud. The 2-1 buydown is a Fannie Mae/Freddie Mac sanctioned method of a seller incenting a buyer when financing is required.

The following example scenario is for demonstration purposes only and will be different for each buyer. This example reflects a purchase price of $750,000 and loan amount of $400,000.

There are other incentives a seller could advertise to attract buyers that may be more attractive and ultimately cost less to the seller. There are other loan products that a buyer might need to pursue given the specifics of their circumstances. Every scenario is unique, and it is important that a buyer’s strategy aligns their circumstances and goals with broader market conditions.

If you know someone thinking about buying or selling and they aren’t sure whether the current market presents the right opportunities for them, I’d love to speak with them.

Share this Post