How Cash Out Refinances are Helping Many Homeowners

October 26, 2023 | Buying

October 26, 2023 | Buying

Most Americans are aware that the Federal Reserve has pushed up interest rates at an unprecedented pace and that inflation continues to outpace wage growth…and some Americans may have learned a couple new combinations of cuss words because of it.

What most don’t understand is how the average household is impacted by these economic conditions through rising credit card rates, home equity lines of credit, and other unsecured debt.

Some families are just looking to tighten the belt and reduce overall payment obligations, others are impacted by financial circumstances beyond their control that might even leave them desperate.

Interestingly though, while mortgage interest rates are higher than we’ve grown accustomed to, many homeowners are actually achieving financial health by refinancing their home, pulling some cash out, paying off debts, and benefiting from the tax deduction of mortgage interest instead of those other dangerous options.

To be clear, I don’t provide financing as a real estate professional, but I believe it is my responsibility to ensure my clients, friends and family are all armed with knowledge that helps them make the wisest decisions. My commitment is to provide perspective on, and be a source of expertise for anything homeownership, finance or wealth building related. Also, I have an elite team of professionals I am surrounded by who help me assess and share this information, and they’re here to partner with me in helping you and anyone you know who might need our help. So that said, let’s dig into some things:

America’s credit card debt is now a record high $1.031 Trillion Fool.com at an average interest rate of 22.76%, according to Wallet Hub, and 28.15% according to Forbes. A congressional report released October 25, 2023, written by the Consumer Financial Protection Bureau CFPB Article states that Americans have paid now a record high $130 billion dollars in just credit card interest and fees over the last 18 months of Federal Reserve rate hikes. (*uncontrollably spits coffee on the computer*)

Home equity lines of credit are now a record high $340 billion dollars at an average rate of 9.02%, and the average car loans are at a balance of $22,612 with a payment of $736.00 per month.

The resulting payments are crushing some households. A credit card balance of $40,000 at a 22.76% interest rate and a starting minimum payment of $1,200 per month (declining over time as the balance decreases) would take just over 30 years to pay off and costs $107,522 in payments.

If the Federal Reserve keeps pushing rates higher, these payment circumstances will only get worse, and we want to help people be informed of their choices.

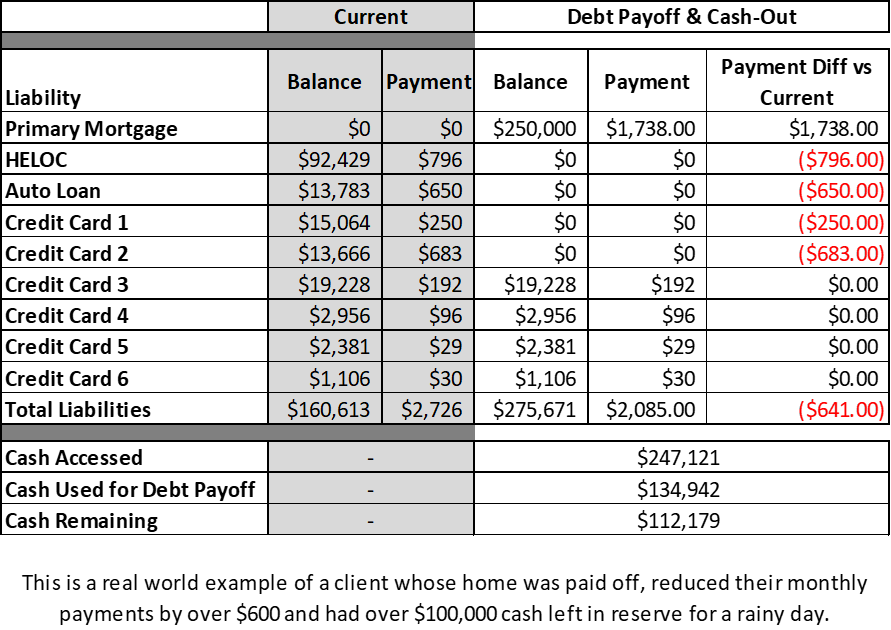

Below is an example of a client who recently approached us asking for help. Fortunately, they weren’t financially desperate, but they understood that the equity in their home was not being put to work for their best good. I referred them to my team to analyze their unique circumstances, run the numbers, and ask questions to help identify what was most important. Then, they executed.

The result? Financial freedom and the liberating feel of a fresh start (maybe some bubbly, but the Costco kind that’s like $20).

Of course, there are varying reasons for household debt. Spending habits get out of control or a family member needs help. Maybe a sudden medical circumstance or a job loss leaves, what feels like, no choice. There is often a weighty shame and fear that comes with living with finances like this, and we’ve experienced some homeowners feeling helpless in similar situations. Our job, more like honor, is to be present as a guide and help people find solutions.

And the truly good news is there’s hope for many, and that hope lives in the asset they already own. Whatever the circumstance, we want homeowners to know that a refinance, which provides the benefit of tax deduction and the payoff of consumer debt, may simply be the wisest and most financially freeing move. No, It won’t be right for everyone, but for some it will be a lifeline.

If you know someone – whether a colleague, your kids, parents, or friends (bingo anybody??) – who has expensive monthly car payments, medical bills, credit card balances, or a home equity line of credit with an interest rate that continues to climb, encourage them to talk to someone who won’t judge their circumstances, but who will analyze their situation and share powerful options.

A quick conversation starting with me might be the best place. I have great business associates such as financial advisors, CPAs, and top of the line mortgage bankers who are expert consultants at their craft. Feel free to have them reach out, or introduce us directly, I’m always here to help.

I hope this finds you well as we all begin to prepare for the holidays (and the dental visits directly following them)!

Share this Post