Colorado Real Estate in 2023

January 12, 2023 | Market Trends

January 12, 2023 | Market Trends

Real estate is the largest asset class in the world.

Residential real estate has been documented as the greatest return on investment asset over the last 150 years (See – The Rate of Return of Everything). In the United States, the real estate industry represents approximately 25% of the country’s gross domestic product annually.

And yet, real estate is much more than an investment strategy or contribution to national economic health. Real estate is where we live our lives. And the importance of our confidence in the value of that asset and its ongoing ability to be the secure place where we live cannot be overstated.

In this annual article, we are going to dive into the unprecedented last 3 years of Colorado real estate. Our goal is to help clients understand the market conditions today and provide clarity to 2023 real estate projections.

These projections include home value appreciation, interest rate movement, buyer and seller motivations, and a quick look at the macroeconomic factors influencing these likely outcomes.

We believe Colorado real estate will be strong in 2023, most likely experiencing a 2-5% appreciation in the first half of the year.

Inventory will remain relatively low as a result of current homeowners’ reluctance to give up their existing low-rate mortgage, and buyer demand is projected to increase as a result of declining interest rates, likely starting in February of this year (See below-Why interest rates will drop).

Total home sales will likely return to just below the more modest 2018/2019 levels, which were very healthy market conditions.

As we have already seen, first-time home buyers will have more opportunities than they have experienced in over 3 years due to greater seller flexibility of contract terms. Expect builders to continue building at a slightly reduced rate from the last two years and to be more aggressive in attempting to attract real estate professionals and their buyers.

While migration to Colorado has slowed over the last two years, a modest increase in population and household formations will further fuel natural demand. And, the ongoing growth of a diversified and strong Colorado economy with unemployment below national levels will continue to position Colorado as one of the country’s top real estate markets.

The second half of 2023 is a foggier picture than the first half of the year.

Concerns of US economic recession driven by the Federal Reserve attempting to control inflation through raising interest rates may drive unemployment to 6% or greater. This, coupled with a very low household savings rate and extremely high household credit card debt may force some homeowners to sell. This could cause the market to reach a tipping point of increased inventory, weakening the current balance of buyer demand and supply of homes and cause a decline in values.

But we don’t think so. The average homeowner in America has 52% equity in their home and a mortgage rate of 3.75% or lower. Rather than excess sellers on the market, we anticipate an increase in the number of homeowners using equity lines to support cashflow when needed and only a very modest increase of forced sales.

We wouldn’t be surprised by a small decline in real estate values in the second half of 2023, as is the natural fluctuation of real estate in Colorado, but analysis of current conditions is most predictive of market stability and modest home value appreciation overall for the year.

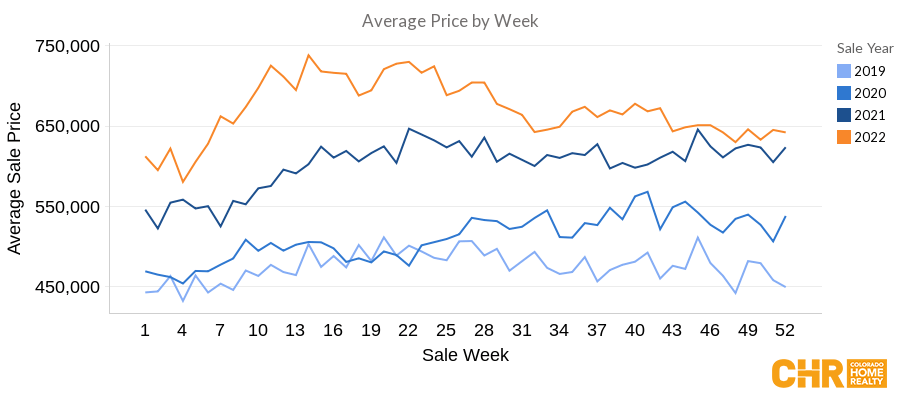

Early 2020 through early 2022 saw two of the busiest and unsustainable years of real estate activity ever recorded in Colorado and the nation. All-time low mortgage rates, population migration, and lifestyle changes drove unprecedented real estate sales volume and home value appreciation.

In April 2020, shortly after mask mandates, mandatory lockdowns, and fear of economic collapse, the real estate market boarded a rocket ship and blasted off. The average single family detached residence in the Denver market sold for $525,000 at that time. Less than two years later, amidst historically low inventory and incredibly strong buyer demand fueled by artificially low interest rates, that average sales price surpassed $830,000. Or $300,000 of equity created per household on average in a two year period.

Over this same period, decades long experiences of price negotiation by buyers and price reductions of overpriced homes by sellers went out the window. If a buyer really wanted to buy, they were in a competitive bid environment, in many cases begging sellers to take their offer.

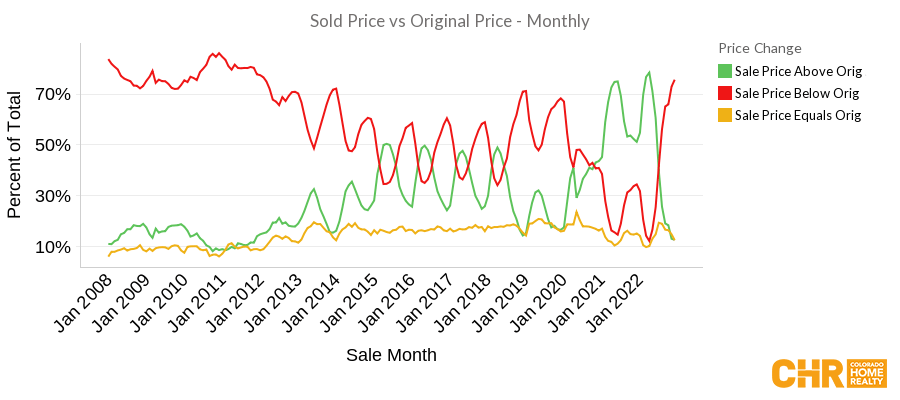

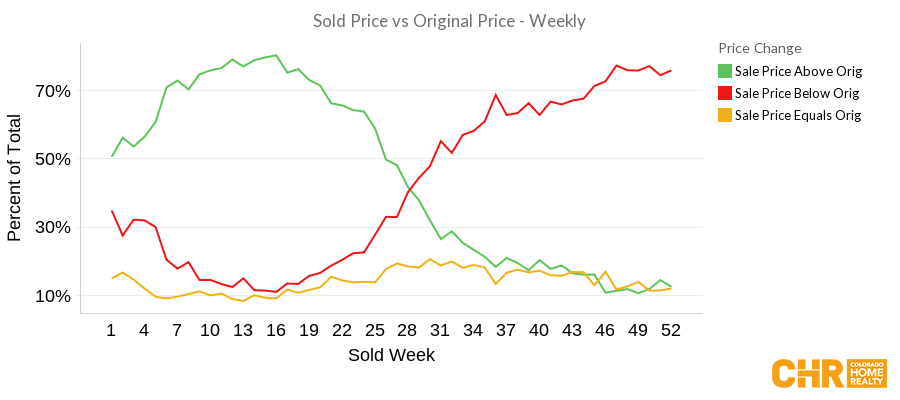

In April of 2022, 78% of all properties sold for more than the seller’s asking price, the highest percentage on record.

Sellers it seemed, couldn’t fail. And, inexperienced and unprofessional real estate agents looked like heroes. Only 5% of all homes listed for sale required the seller to reduce the price before going under contract.

Then it happened. Challenged supply chains. Prolific government spending flooded the economy with money. Artificially suppressed long term interest rates.

A price had to be paid.

Interest rates are directly tied to inflation and in mid-2021 the US economy began feeling the effects of inflationary pressures. As inflation measures rose, interest rates began a shift in trajectory. By early 2022, what was once historically low became the fastest rise of mortgage interest rates ever seen.

What immediately followed was only too predictable.

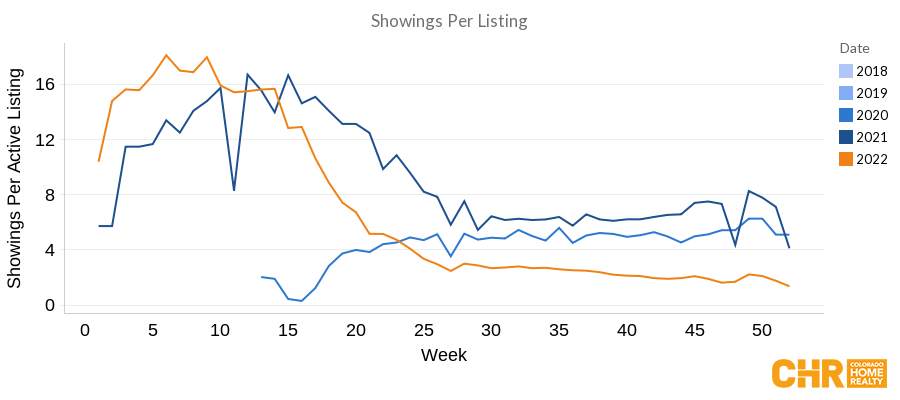

As mortgage rates rose from 3.25% in early 2022 to as high as 7% in November, we saw buyers withdraw from the emotional and practical increased cost of homeownership.

Commensurately, sellers saw an unprecedented decline in buyer activity. In early 2022 sellers experienced an average of 18 showings per week on their for-sale home. By year-end, that number declined to 1.3 showings per week.

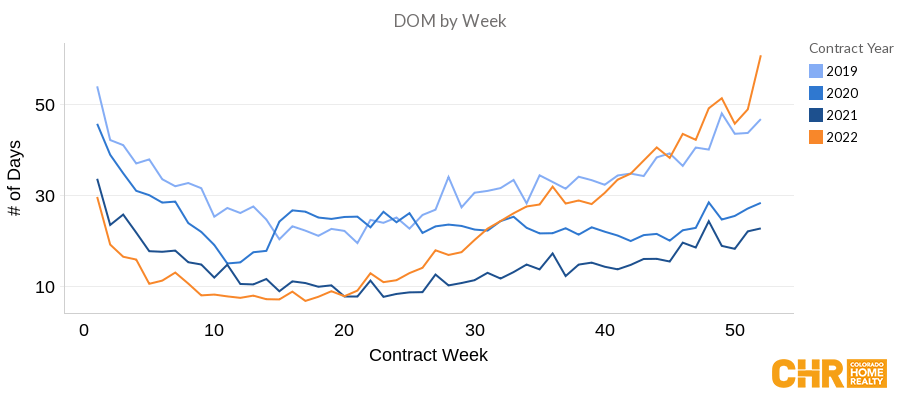

Homes that were under contract in an average of 7 days on the market (DOM) in March of 2022 moved to over 64 days by year-end.

What had previously been 11.5% of properties selling for less than the asking price in the Spring moved to over 80% selling for less than the asking price by year-end.

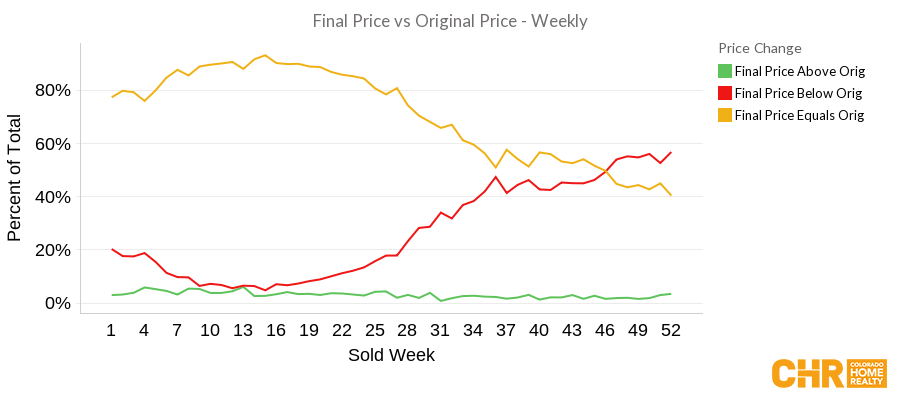

And what was a low of 4.8% of properties experiencing a price reduction moved to 62%.

Buyers were frustrated by rising mortgage rates, and sellers were mad and maybe a little scared that their homes were not going under contract in 10 days. Homes were being overpriced due to an emotional conviction by sellers and unaware real estate agents, that things couldn’t change this fast.

Inexperienced or unprofessional agents started getting out of the business, incapable of consulting, guiding, and leading their clients through these changes.

Sales volume and home value appreciation came back to earth, ending the year with approximately 48,000 homes sold in 2022 versus almost 60,000 just one year prior. And 2022 ended with an average single family detached residence selling for just over $712,000 in the Denver metro area.

For the most part, the simple economic principle of supply and demand drives the rate of appreciation in the housing market. In real estate, supply is the number of homes that come available for sale and demand is the number of buyers wanting to buy.

What drives buyer activity is a combination of economic security and the cost of capital to acquire a home relative to the cost and inconvenience of renting. Or simply put, interest rates and monthly payment versus rental rates and insecurity.

While we acknowledge the economic insecurity of the long-term employment market and inflation concerns, interest rates in 2023 are most likely coming down which will boost buyer activity. This boost of buyer activity is an increase in demand, putting upward pressure on home prices if there isn’t a significant rising in supply.

Sellers are motivated by security and lifestyle change. The combination of economic uncertainty, more than 50% equity in their current home, and low interest rates on their current home mortgage, fewer sellers are likely to view the market conditions as a time to make extravagant purchases. This most likely results in keeping the supply of homes relatively low.

We do anticipate inventory surpassing levels seen in the last decade, but this will only serve to slow the market down, create a nicer pace of property searching for buyers, minimize the chaos and frenzy for sellers and keep the home value appreciation rate closer to historical norms.

Homeowners who want to sell can be much more confident in finding a replacement home and negotiating terms that allow for an easier transition from one home to another, than the last few years.

Mortgage Interest rates are almost directly tied to the rate of inflation. Essentially as inflation increases, mortgage rates increase and vice versa.

The most common measure of inflation is the consumer price index (CPI) and the CPI is calculated on what’s called a 12-month moving average. This 12-month moving average is calculated monthly on the cost of 8 categories of consumer expenses averaged over the previous 12 months.

The 8 categories of CPI calculation are:

The cost of housing is the most significant portion of the CPI making up 39% of the total calculation. And the housing portion of the calculation is measured as the rate of increase of rental property monthly cost by consumers.

Stick with us here, we are getting to why mortgage rates will drop!

12 months ago, the cost of rent was increasing at an annualized rate of almost 18%. At that time, the cost of gas and food were also rising at a significant rate.

And, shortly thereafter was watched interest rates rise rapidly.

Even though the cost of food has stabilized, and gas and housing have come down markedly, the high pace of increase from 12 months ago is still calculated into the inflation rate today, thus keeping mortgage rates inflated.

As you can see from the chart below, the cost of rent increase came down to 4.6% in November and is now down to 3.4% as of December of 2022 (not shown in the below chart). But the 12-month moving average calculation still includes the 18% year-over-year rental rate increase from January of 2022.

As CPI is recalculated in February of this year, eliminating the highest rental rate increases from 13 months before, we will see the beginning of a decline in the CPI measures.

As the CPI measure declines, we will see a correlated decline in mortgage rates.

One significant market characteristic we are watching is the cost of energy. Both domestically and internationally there continues to be upward pressure on energy prices driven by a combination of policy changes, international consumption, and availability.

China is the largest importer of energy in the world and their economy has been all but shut down for the last two years. If China opens back up, more demand will be placed on an already reduced worldwide energy supply, potentially driving prices higher.

The rising cost of energy is in and of itself about a 13% contributor to the inflation calculation. But as importantly, the rising cost of energy significantly impacts the availability and cost of food production and transportation. The cost of food is an 11% contributor to the CPI calculation.

Not only will these costs affect the CPI calculation, influencing the rise or fall of mortgage interest rates, but the rise or fall of these expenses will impact the average household’s savings rates and ultimately disposable income to purchase homes.

With all of that, we still most likely see 30-year fixed mortgage rates back in the high 4% to low 5% range.

While there are a number of wild cards that may impact the direction of the US economy and the resulting housing market, the balance of buyer demand and seller supply will likely create a stable and modestly appreciating US housing market for 2023.

With mortgage interest rates likely declining over the next 6 months, we anticipate a busy spring selling season in Colorado.

There is only one category of consumer we recommend staying away from a real estate purchase right now and that is someone whose household does not have at least 6 months of cash in reserve after purchasing a home and/or is in an industry that has proven to be particularly susceptible to these changing economic conditions. We anticipate upward of 7 million more Americans losing their job over the next 15 months. Our job is not to sell real estate. Our job is to impart wisdom and perspective to help our clients live well.

While it may seem self-serving to say so, market conditions are great for Buyers to purchase a home right now. While interest rates are a bit higher at the moment, that is keeping some of the uneducated or scared competition away. A great strategy is to purchase now before we see the spring market appreciation and refinance as rates drop. You’ll get the best of both worlds; a slightly lower purchase price and better contractual terms today and likely lower interest rate in just 6 months.

Sellers should be confident putting their home on the market and finding a replacement home. Sellers will enjoy modest market appreciation this spring, days on market coming down, slightly reduced need for negotiation with buyers and the pace of the market will allow for sellers to find a replacement home and ease the transition to a new property.

Sellers should prepare for:

Buyers need to expect:

Share this Post